On last night’s Fast Money on CNBC we opened the program with a discussion of whether or not investors looking to put fresh money to work in the stock market should stick with winning sectors year to date or dabble in with some laggards. While my crystal ball is in the shop for a tune-up, I thought I’d riff on this topic for a minute.

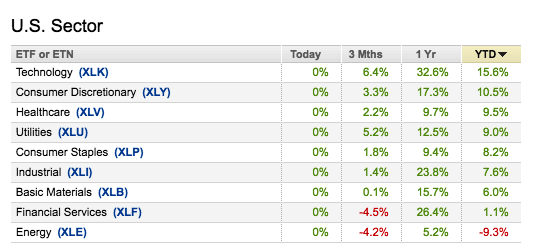

First, let’s take a quick look at the ytd performance of the major S&P 500 sectors:

The obvious outperformance in Tech and Consumer Discretionary is lead by a handful of tech(ish) stocks that make up a disproportionate amount of both sectors, while also fueling the massive outperformance of the Nasdaq Composite’s (up 14% ytd) vs the S&P 500 (up nearly 7% ytd). Again, the Nasdaq’s heavier exposure to the five largest companies in terms of market cap in the U.S., Apple, Amazon & Facebook (all up 30% in 2017) and Alphabet and Microsoft (up 21% and 10% respectively) are the cause. Mega-cap tech feels a bit like a safety trade given their strengthening monopolies, outsized growth, strong balance sheets, massive cash generation and likely to be the single largest beneficiaries of what is likely to be the only legislative reform to get done in 2017, offshore cash repatriation.

Surprisingly the next three, Healthcare, Utilities and Consumer Staples, may be viewed as defensive, and in the case of Healthcare possibly just a dead cat bounce, or the optimism about less regulation under the current administration. As for Utes and Staples, maybe the continued low rate environment is causing investors to view as a bond proxy and the surprising weakness year to date in the dollar could be a boon for the likes of J&J and P&G.

Industrials and Basic Materials have kept pace with the S&P 500 since the election, but have not outperformed, possibly a reflection of investors skepticism about a dramatically improving economy in 2017 and the unlikelihood that any material infrastructure legislation gets passed soon.

Financials, a disaster in my mind. The initial outperformance of U.S. bank stocks after the election displayed hope among investors that the new president would stimulate the economy and roll back financial crisis regulations that hampered bank stock revenues and profitability. The massive underperformance since March 1st, down 7.5%, vs the SPX that is basically back at the prior all time highs made that day suggest investors see risk to any meaningful changes to Dodd-Frank and the unlikelihood of rates going much higher anytime soon.

And Energy, what can I say, crude should be acting better when you consider the weakness in the U.S. dollar, OPEC output deals and the rumblings of global economic reflation. But its acts like death.

All that said, the SPX is at prior highs, looking poised to breakout, with volatility readings very near 52-week lows. But here is the thing, and I ain’t wish-casting, can you price in the potential risks to US growth as the White House is likely to spend at least the balance of the year in scandal defense mode? I cannot. But we’re already in the middle of a political storm, and it is likely to table most of the proposed legislative agenda that so many investors, Red or Blue have been banking on since late 2016. Newsflash, they ain’t coming, not in 2017 and if that is why you bought stocks over the last 6 months it may be time to rethink the thesis.

This look under the hood isn’t great, despite the year to date gains.