Yesterday the Lex column in the Financial Times ran an interview with Square’s (SQ) CEO Jack Dorsey (here). The interview was primarily focused on Sqaure’s launch in the U.K. but the conversation quickly turned to his other company Twitter, and the synergies of a merger between a payments processing company and a social networking/ short messaging company (Dorsey founded Twitter and is the current CEO).

Aside from solving the obvious problem of fending off activist investors (rumored to be on the prowl in TWTR) looking to make Dorsey choose one or the other companies to run, the best reason for such a combination:

In a world where offline spending data could be linked to online profiles, Twitter would benefit from better ad targeting,

This is the holy grail for all social media companies, to better serve ads based on your actual shopping habits, both online and in the real world. But it’s not necessarily that easy for a company like Twitter:

but that particular privacy Rubicon seems unlikely to be crossed. Most problematically, the companies that use Twitter most enthusiastically are large, and businesses that use Square tend to be small.

On a few occasions over the last year I have made the case for similar combinations, thinking back to how Facebook (FB) hopes to monetize their $20ish billion acquisition of short messaging service WhatsApp. Soon after the deal closed in 2014, Facebook hired David Marcus, who at the time was CEO of PayPal (PYPL). They are not going to jam adds on WhatsApp, they are going to use at as peer to peer or business to consumer payments mechanism. That makes perfect sense.

For investors, there is very little to get excited right now in TWTR stock. One might have thought the comparative valuation of Snap Inc (SNAP) as a public company would have tech investors appreciate the scarcity value of an established social media company like TWTR (320ish million monthly active users) that sports an enterprise value less than $9 billion (3.5x trailing 12 month sales vs SNAP at 13x expected 2017 sales). But they haven’t. Twitter management needs to change the narrative of the story, and quick, because Q4 results showed better monetization on existing users, but still anemic user growth. That’s not gonna cut it.

Fundamentals aside, there are a couple ways to look at this stock chart. With sentiment so poor (11% short interest and only 5 buy ratings, 20 holds and 14 sells on the stock) a lot of bad news might be in the stock, down 80% from its 2013 post-IPO highs, and just a few percent from its all-time lows:

But looking at it another way, the prior lows look like a sort of do or die line in the sand as they are the neckline for a textbook head and shoulders top:

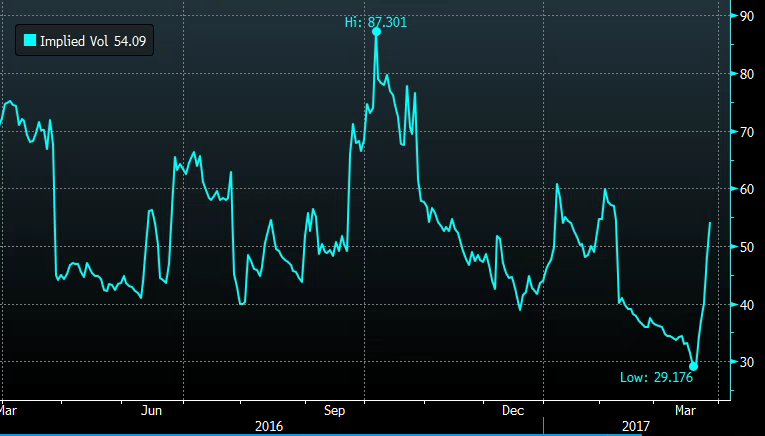

While there appears to be little panic in the options market for most U.S. stocks, short dated options prices have spiked fairly dramatically of late:

For those who are looking to be contrarian, we continue to think it makes sense to sell downside puts to buy out of the money calls or call spreads spending little in premium but offering leverage to a sharp upside move.

Most smaller social media properties would dream of a combination with an established payments processor. Twitter is at an obvious advantage in this department due to their CEO’s rare role with both comapnies . So keep an eye on @Jack’s calendar in case he schedules a meeting with himself. I suspect a merger between TWTR and SQ would be viewed very positively by investors.