MorningWord 2/28/17: In Like a Lamb, Out Like a Lion?

by Dan February 28, 2017 9:42 am

• FREE ACCESS

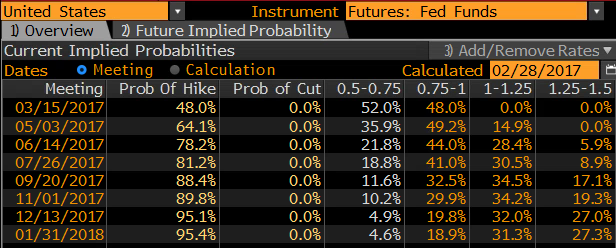

Yesterday over at the Boock Report, Peter Boockvar highlighted the rising expectations for a Fed Fund rate hike at the March 15th FOMC meeting:

The April fed funds futures contract which fully captures the March meeting is now pricing in a 44% chance (using the midpoint between .50-.75% instead of the current effective rate of .66%) of an interest rate HIKE at that get together. That level was seen on February 15th the day after Yellen’s testimony and June 2016 before that. Rate hike odds were 24% three weeks ago. In the Fed’s desire not to surprise markets as Loretta Mester repeated last week, hike odds anywhere close to 50% would give them cover to go. We think they do.

Bloomberg

Let’s not forget, Goldman Sach’s research shows historically, the Fed does not like to surprise market participants on hikes:

going back to 1994, 90 percent of the 31 rate hikes were priced in at least 50 percent 30 days ahead of the FOMC meeting. Getting closer to the meeting, the median hike was 95 percent priced in, with only a few deviations, such as from the Alan Greenspan Fed in March 1997 and November 1999.

The options market is implying only a 1.6% move in the SPY between now and the March 15th close, or a $3.86 (the March 15th 237 call premium + put premium) move in either direction (based on a $237.11 close yesterday.) Normally, if you were to that you could risk less than 1% for at the money long exposure or protection into an uncertain market event like a somewhat surprising Fed rate hike, I’d tell you that your nuts!

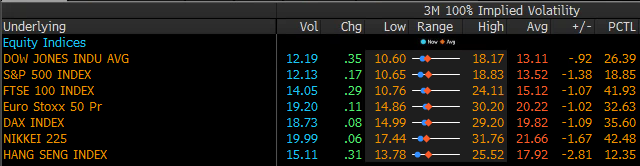

And it’s not just here in the U.S. but global equity markets are trading at implied volatility levels well below their norm, per Bloomberg:

As we tune into watch the new President’s prime time speech this evening to Congress, its important to consider the expectations that investors have already priced in (SPX up 10% since the election, a 15% reversal from the Nov 8th overnight lows). And give some serious non-partisan thought to the complexity of implementing campaign promises the market has already assumed, like tax reform and a budget that does not result in a larger deficit. But then remember that the more protectionist aspects of the campaign affecting foreign policy, immigration, movement of labor, and renegotiating trade deals with the developing world have yet to get their day in the sun. Unless the market is pricing in an assumption that all of this complexity will cancel each-other out and the only thing we’ll be left with is lower taxes and gutted regulatory agencies like the EPA, SEC, NLRB and FTC, I assume all of this uncertainty during both a political and a central bank transition will get volatility off the mat.