MorningWord 4/3/13: At this stage of the bull market, as the Dow and the SPX make new all time highs on a daily basis, it is gonna take a bit more than dart throwing on the long side of the trade to eek out significant relative out- performance. As multiples of single stocks keep expanding, bulls have migrated from the tagline “equities are cheap relative to…….” to now identifying most attractive longs as “growth at a reasonable price”. There is an important distinction to be made btwn these two comments, the first statement was likely true on a relative basis compared to most other risk assets, and the latter is just a way to help those sleep at night for owning equities that did not fit their value criteria at earlier stages in the bull run. Whatever you tell yourself to justify owning a stock whose run may be long in the tooth is fine with me, but managing risk at highs can be one of the most important investment decisions you ever make.

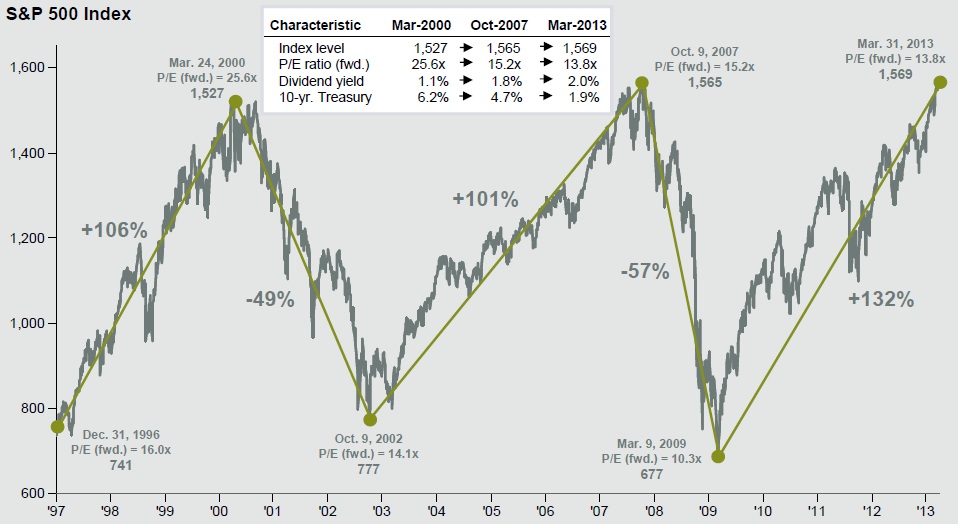

Barry Ritholtz of the Big Picture Blog yesterday ran the chart of the SPX since 1997 (below). We have posted similar charts in the recent past showing the great bull runs and 50% re-tracements from the highs, but this one is just so neat.

Equities remain resilient to say the least, but we keep seeing noticeable divergences and what appears to be slowing momentum in the broad market. On Twitter yesterday, Enis noted, “NYSE Advancers closed below 1500, but SPX finished up 0.5%, quite rare to see divergence that big. IWM also -2% vs. SPY this wk”. (follow Enis on Twitter @EnisTaner as he plans to be more active wtih his macro musings).

The SPX continues to show massive out-performance to almost every major equity index the world over (ex-Japan, the Nikkei is up ~19% ytd), which should worry bulls that the “SPX Flight to Safety” trade is becoming a tad crowded. In 2009 the global economy was bailed out by the reflation of emerging market demand, but if emerging market equity indices like Brazil’s Bovespa (down ~9% ytd), China’s Shanghai Comp (down ~2% ytd) and Russia’s Micex (down ~3% ytd) are telling us anything, we will need a different catalyts this time around at a time when European growth is clearly struggling. It can’t all be left to U.S. Federal Reserve.

SO we remain fairly cautious heading into Q1 earnings season in the coming weeks, but recognize the potential for a breakout of the 25 point range the SPX has traded in over the past month. A run to 1600 could clearly be in the cards, and to be perfectly frank there is no resistance overhead, aside from the top of the trend channel that has been in place off o the 2009 lows.

[caption id="attachment_24336" align="aligncenter" width="589"] SPX 5 yr chart from Bloomberg[/caption]

SPX 5 yr chart from Bloomberg[/caption]

As I said Monday morning in this space:

the SPX continues to levitate, and it does so now with a new high under its belt at the start of a quarter that could see meaningful capital inflows. So early this week I think it makes sense to stay out of the way, and see what they got so to speak. But if we are going to continue to make higher highs, we will need to see broader participation from less defensive sectors, and banks and tech will need to break out of its funk. Q1 earnings and Q2 guidance will be the next driver for U.S. equities.

If you think you missed the U.S. equity party and are dying to get in, I assure you your PnL will thank you for defining your risk with calls or call spreads with implied volatility as low as it as, rather than committing new capital to outright long positions. While the the price action in equities may stay a tad irrational for the time being, the reaction to Friday’s Jobs Report may be the tell for the short term.

Jerry Maguire: Breakdown? Breakthrough

[hr]

MorningWord 4/2/13: Yesterday I read an interesting post on Barron’s Tech Trader Daily Blog detailing a research note from a MS hardware analyst Huberty titled, “HPQ: New Exec Incentives Could Boost Cash, Says Morgan Stanley”. The gist of the story is that HPQ dramatically lags industry peers in cash management, particularly conversion cycles and days sales outstanding, which, if fixed, could cause positive cash flow revisions to street consensus. Investors in DELL back in the 90s learned that the stock wasn’t a great investment because it made the best computers, but in large part they gained an edge vs their peers as a result of mastering the logistics of making computers, which had very positive financial implications.

HPQ has either been too big, too lazy or outclassed on the management front to achieve anywhere near industry averages (days sales outstanding for HPQ were at 48 days last qtr vs AAPL, DELL, & Lenovo at 33 days for PCs and Cash Conversion cycle at neg 35 days vs HPQ at plus 14—per MS). What I found most interesting about MS’s take (after recently upgrading the stock to a BUY with a $27 price target) is that “HP’s revised FY13 executive compensation structure includes incentives based on ROIC and FCF metrics. Prior plans only rewarded executives based on revenue and earnings as well as individual goals. Under the new structure, HP’s compensation committee specifically highlights a focus on “cash management practices, including working capital and capital expenditures”

While these sort of compensation incentives may be common for turnaround situations, it smacks of some of the incentives that Wall Street bankers had in the middle part of last decade, and we all know how that ended.

HPQ is a bit of an enigma of a stock here after being the worst performer in the Dow last year, is the best in 2013, can u scream DOG OF THE DOW! The stock’s 105% rally off of the 1o year lows makes for an interesting technical set up. On a near term basis the stock is quickly approaching massive resistance at the $25 level and appears to be fairly overbought.

[caption id="attachment_24293" align="aligncenter" width="589"] HPQ 2 yr chart from Bloomberg[/caption]

HPQ 2 yr chart from Bloomberg[/caption]

On a long term basis, November’s low should serve as the mother of all double bottoms!

[caption id="attachment_24294" align="aligncenter" width="589"] HPQ 30 yr chart from Bloomberg[/caption]

HPQ 30 yr chart from Bloomberg[/caption]

The stock’s 64% gains year to date and only 3% short interest demonstrates a fairly large divergence btwn investor sentiment and that of Wall Street analysts who have 6 Buys, 21 Holds and 10 Sells on the stock with an avg 12 month price target of ~$18.50. Analysts do expect 2013 to be the trough for earnings, and returning to low single digit growth in 2014. I guess the obvious question is what sort of recovery and turnaround is already priced into the shares at current levels?? We are keeping a close eye on this one, particularly from a vol perspective as IV nears 52 week lows.

[hr]

MorningWord 4/1/13: Q1 2013 was some quarter for investors in U.S. equities on an outright basis, and relative to almost every other equity market the world over (ex Japan up nearly 17% ytd!). While I had a sneaking suspicion that the combination of a holiday shortened week and quarter-end window-dressing would get us to the all time high in the SPX, I didn’t think we would close the quarter on what amounted to the DEAD-ASS HIGH. The powers that be just couldn’t help themselves knowing that many market participants were observing Holidays/Spring Breaking, but the real test for the strength of the rally will come as we get into the meat of Q1 corporate earnings in the next couple of weeks.

As Josh Brown of The Reformed Broker blog commented (read here) via FactSet research (read here), negative earnings pre-announcements have been running hot:

For Q1 2013, 86 companies have issued negative EPS guidance while 24 companies have issued positive EPS guidance. As a result, the overall percentage of companies issuing negative EPS guidance to date for Q1 2013 stands at 78% (86 out of 110). If this is the final percentage for the quarter, it will mark the highest percentage of companies issuing negative EPS guidance since FactSet began tracking guidance data in Q1 2006.

While I would love to pound the table and suggest this is a bad omen for earnings season, it is hard to make the case as it is backward looking and does not account for the potential for better than expected forward guidance. Investors appear to be more focused on what they perceive to be the gradual improvement in housing and employment than that of the financial performance of individual companies as it has become most popular to choose from one of many excuses for one off misses (Sandy, Fiscal Cliff, and always Europe). IN the case of ORCL just 2 weeks ago, the company issued disappointing earnings and sales, but suggested this was the result of poor execution by their sales force and they are likely to close much of the business they missed of late in the current quarter……suggesting an earnings beat in the near future?

Make no mistake about it, the SPX is at a difficult technical spot for the bears. Thursday’s close of 1569.19, the new all time closing high, after more than 3 weeks of basing above 1540, could suggest a sort of blow off situation to the upside.

[caption id="attachment_24232" align="aligncenter" width="589"] SPX March 2013 from Bloomberg[/caption]

SPX March 2013 from Bloomberg[/caption]

As I fall into the bear camp, I have done so in a fairly cautious manner, with small positioning, more from a probing standpoint, rather than going all in. While I am not a fan of the near term fundamental backdrop for equities in their current state, I remain a bit fearful in the coming week of the chart below of the SPX, popping out of the Flag formation, in a period that could see reasonable inflows at the start of the quarter, and in a period that could see light news flow prior to earnings season (despite a trickle of pre-announcements).

[caption id="attachment_24233" align="aligncenter" width="589"] SPX 1 yr chart from Bloomberg[/caption]

SPX 1 yr chart from Bloomberg[/caption]

BUT, there are a few things that are making me nervous about the internals near-term, most importlanty, the sectors that got us here YTD, don’t exactly scream BULL MARKET. As JC Parets from the AllStarCharts blog last week pointed out (below), defensive sectors like consumer staples and utilities, the 2 best performing sectors in the S&P have been doing much of the heavy lifting ytd.

[caption id="attachment_24234" align="aligncenter" width="594"] Leadership-Stays-Defensive-in-2013-All-Star-Charts-All-Star-Charts[/caption]

Leadership-Stays-Defensive-in-2013-All-Star-Charts-All-Star-Charts[/caption]

So the obvious observation would be, when do Financials and Tech join the party? The recent loss of momentum in U.S. bank stocks should be of particular worry at a time where the SPX and the Dow are making all time highs. MS looks particularly vulnerable in my opinion, closing Thursday down ~10% from the 52 week highs made in Feb and sitting right on important technical support.

[caption id="attachment_24235" align="aligncenter" width="589"] MS 1 Yr from Bloomberg[/caption]

MS 1 Yr from Bloomberg[/caption]

Thursday’s price action in AAPL (down 2%) and GOOG (down 1%) was interesting, as many market participants were convinced that AAPL had bottomed last week, and that GOOG was infallible. I am not in the camp that AAPL has bottomed, but GOOG’s break below $800 on decent volume could have marked a near term top of a stock that was an obvious recipient of AAPL’s recent pain.

[caption id="attachment_24236" align="aligncenter" width="589"] GOOG 1yr from Bloomberg[/caption]

GOOG 1yr from Bloomberg[/caption]

So to sum up, the SPX continues to levitate, and it does so now with a new high under its belt at the start of a quarter that could see meaningful capital inflows. So early this week I think it makes sense to stay out of the way, and see what they got so to speak. But if we are going to continue to make higher highs, we will need to see broader participation from less defensive sectors, and banks and tech will need to break out of its funk. Q1 earnings and Q2 guidance will be the next driver for U.S. equities.